Key takeaways

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

- Stock management keeps cash flow healthy and customers happy

- Forecasting and FIFO reduce waste and boost profit

- Automating stock control saves time and increases visibility

- ABC analysis helps you focus on your most valuable stock

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Effective stock management is vital for all businesses. Whether you run a local shop, an online store, or work in any industry, managing stock well helps you stay competitive, minimise waste, and keep up with customer needs.

This guide explains what stock management is, why it matters for small businesses, and how to manage inventory effectively.

We'll explore the benefits, common challenges, proven methods, and tools that can make stock control easier and more profitable.

Table of contents

- What is stock management?

- How to manage stock effectively

- Common stock management challenges

- Tools and technologies for stock management

- Stock control methods: four main types

- How cloud-based inventory systems boost efficiency

- HOLD: Premium Business Storage in London

What is stock management?

Stock management refers to the process of ordering, storing, tracking, and controlling a company's inventory. It ensures you always know your stock levels and have the right amount of stock available to meet customer orders without tying up money in unsold goods.

Stock management vs inventory management

While people often use the terms interchangeably, inventory management typically encompasses the entire cycle of raw materials, work-in-progress, and finished goods.

On the flip side, stock management focuses more on finished products ready for sale.

Why does effective stock management matter for small businesses?

Good stock management improves cash flow, helps avoid overstocking or stockouts, and ensures customers get what they need when they need it.

It also reduces waste and storage costs, making business operations more efficient.

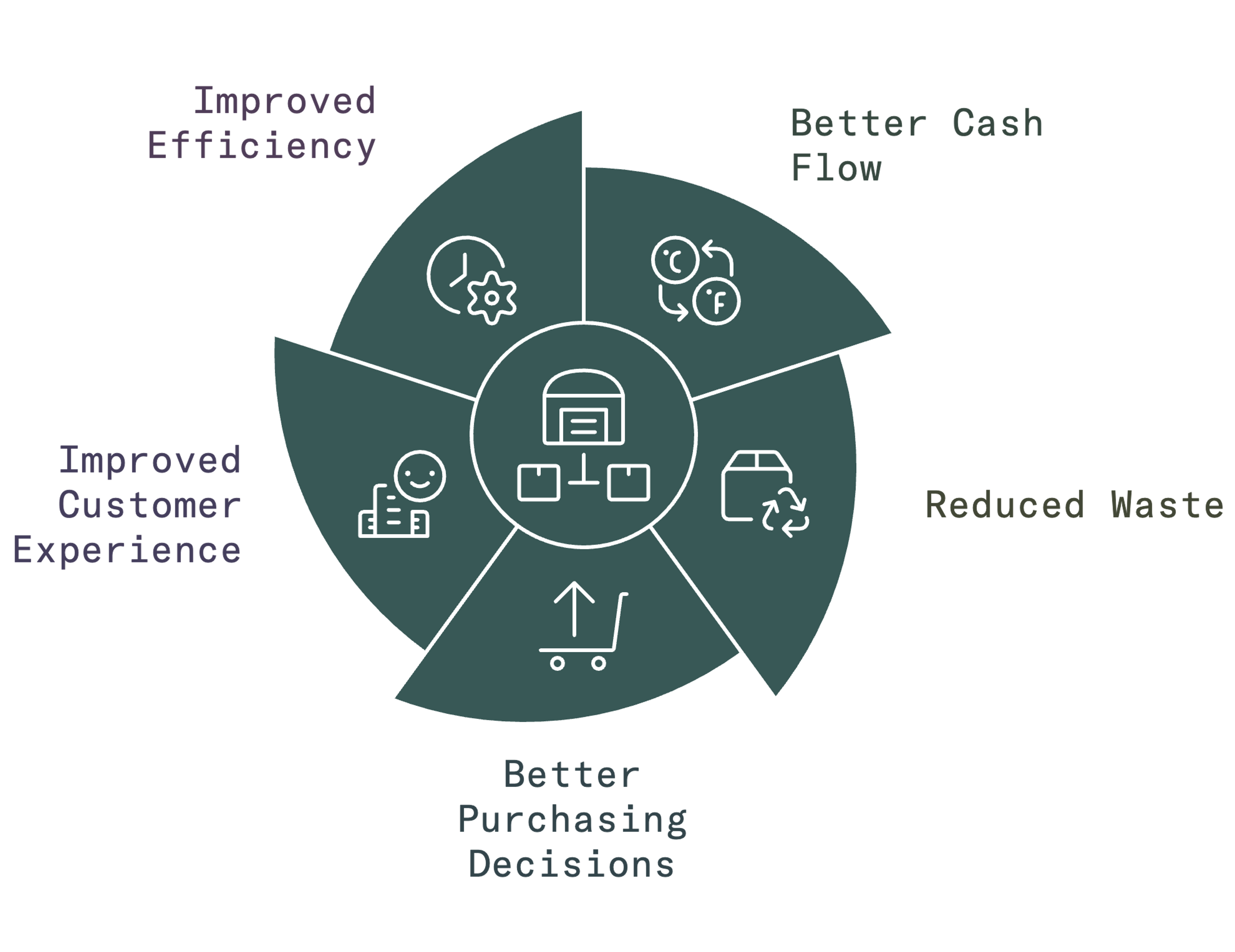

Benefits of effective stock management for small businesses

Better cash flow: Accurate stock control prevents you from overspending on items that don't sell quickly. This frees up money for other parts of your business.

Reduced waste: Using methods like FIFO (First-in-first-out ) helps ensure older stock sells first. This helps prevent spoilage and obsolescence, which is especially important for perishables and seasonal goods

Better purchasing decisions: Tracking sales trends helps you forecast demand and order the right amount of stock at the right time.

Improved customer experience: Having popular products in stock means you can process orders promptly and meet promised delivery times, which builds customer trust and loyalty.

Improved efficiency: Modern systems reduce manual tasks and human errors, saving you time and improving operational efficiency through real-time data for smarter decision making.

Effective stock management allows businesses to respond quickly to customer demand changes and maintain smooth operations.

Common stock management challenges

Managing stock comes with challenges, especially for small businesses with limited resources.

Overstocking and stockouts

Keeping too much stock ties up money and storage space, and excess stock may not sell in time, especially with seasonal items. Holding too little stock saves money up front but increases the risk of running out and missing sales if suppliers are delayed.

Tip: Balancing stock levels carefully helps avoid both problems.

Perishable vs non-perishable goods

Perishable products like food, flowers, or pharmaceuticals require stricter tracking and faster turnover to avoid spoilage and waste.

Non-perishable items still face risks if they sit too long: they can become outdated, damaged in storage, or hard to sell once demand changes.

Tip: A good stock rotation plan helps manage both types.

Manual tracking errors

Relying on spreadsheets or paper records increases the likelihood of data entry errors, duplicate orders, or overlooked stockouts. These errors can disrupt your production process and lead to missed sales or overstocking.

Tip: Switching to a digital stock management system helps keep records up to date automatically.

Poor forecasting

If your sales forecasts are inaccurate, you may order the wrong amount of stock: either too much or too little. This creates waste, cash flow problems, and delays in fulfilling customer orders.

Tip: To improve forecasts, review historical sales data, watch market trends, and adjust predictions for seasonal spikes.

Damage or theft

Damaged or stolen stock can reduce profits and often goes unnoticed without regular checks. Small businesses should inspect deliveries upon arrival, store valuable items securely, and utilise CCTV or access controls where feasible.

Tip: Insurance and clear staff policies also help protect inventory from loss.

How to manage stock effectively

Follow these practical steps to improve your stock control processes:

1. Choose the right inventory method

Decide which stock control approach suits your business. Many businesses use FIFO, JIT, or EOQ. For example, FIFO ensures the oldest inventory is sold first to prevent spoilage and obsolescence.

2. Forecast accurately

Use historical sales data, seasonal trends, and customer behaviour to predict demand. Accurate forecasting helps avoid excess inventory and stockouts.

3. Use ABC analysis

Categorise stock into three categories: A (high-value items), B (moderate value), and C (low-value). Focus more effort on monitoring A items since they contribute most profit, and manage less popular items carefully to avoid overstocking.

4. Set stock levels and reorder points

Decide on a clear minimum stock level and maximum stock level for each product. Automate reordering when stock drops below the minimum stock level.

5. Use inventory management software

Cloud-based software keeps everything updated across multiple channels and locations in real time.

6. Review and fine-tune regularly

Check stock data often to spot changes in customer demand or supply chain issues. Adjust your processes to stay competitive and efficient.

Tools and technologies for stock management

A stock management system helps businesses keep a real-time record of all their products, making it easier to track stock levels and avoid errors. Investing in the right stock management system is a smart move. Here’s what to look for:

Automation and real-time data: Reduces manual work and keeps stock amounts accurate.

Cloud-based access: Manage your stock from anywhere and sync data across multiple locations.

Integration: Connect your stock control system with sales platforms, couriers, and accounting software.

Popular software solutions in the UK: Look at options like Zoho Inventory, TradeGecko, and QuickBooks Commerce. These systems offer good inventory management for small businesses.

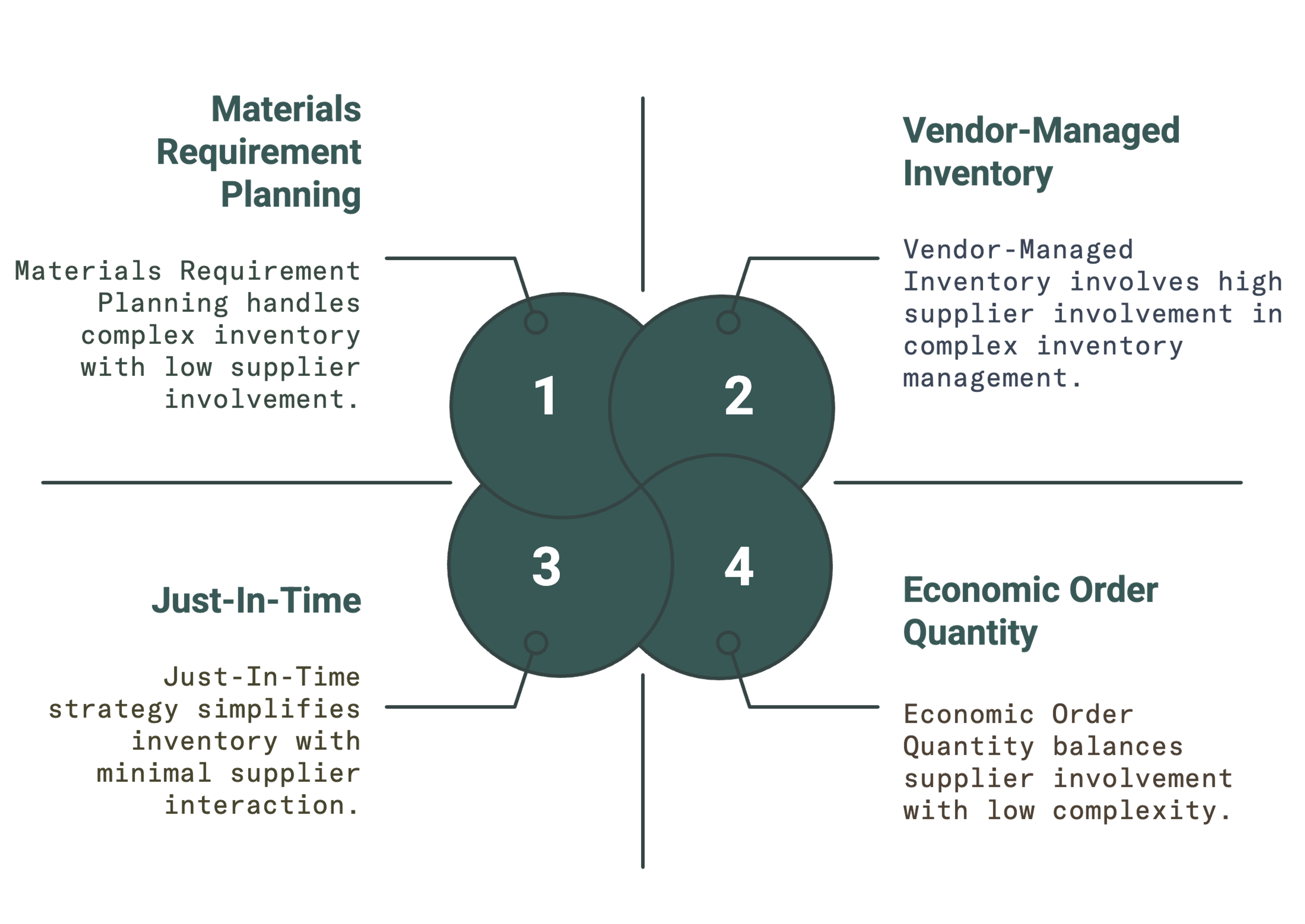

Stock control methods: four main types

Small businesses can use different methods to manage inventory and keep operations cost-effective. The four main types are:

Just-In-Time (JIT)

This approach orders stock only when needed, which lowers storage and insurance costs. JIT is helpful for businesses with reliable supply chains and fast production processes.

Economic Order Quantity (EOQ)

Economic order quantity (EOQ) calculates the optimal number of units to order at once to minimise total inventory costs.

Vendor-Managed Inventory (VMI)

Vendor-managed inventory (VMI) allows suppliers to manage the inventory levels for a buyer at the buyer's location. This ensures timely deliveries and reduces the risk of stockouts.

Materials Requirement Planning (MRP)

MRP utilises sales forecasts and production schedules to maintain accurate inventory levels. It is especially useful for companies that manage raw materials and finished goods in a complex production process.

Combining these methods with good forecasting and accurate stock levels helps small businesses avoid under-stocking, surplus inventory, and costly mistakes.

How cloud-based inventory systems boost efficiency

Manual stock management is time-consuming and error-prone. Modern stock management systems provide better inventory visibility and control for businesses of any size.

These systems do more than store data: they also connect with couriers and sales platforms to streamline order fulfilment and delivery tracking.

Features and benefits

- Integration with point of sale: Many inventory management systems integrate directly with your point of sale to automatically update inventory levels.

- Cloud-based tracking: Cloud-based software enables business leaders to track stock across multiple locations and channels in real time.

- Smart forecasting: Integrating machine learning and advanced data tools helps companies forecast demand and fine-tune stock control.

- ERP systems: ERP systems integrate sales, purchasing, stock control, and other business functions to give managers a complete view of the supply chain.

Inventory management software makes it easier to manage stock based on current demand. This avoids tying up money in unsold goods and keeps fulfilment processes running smoothly.

Conclusion

To keep a retail business agile, you need good stock management. Using proven methods like JIT, FIFO, EOQ, and modern software solutions helps your business control costs and meet customer demand.

We can't stress this enough: always protect your stock. Damage or theft can hit your bottom line hard. Using a secure storage facility like HOLD (with 24-hour surveillance and access controls) reduces this risk and provides peace of mind.

HOLD: Premium Business Storage in London

HOLD is a modern storage provider on a mission to transform self storage in London. Our business storage solutions offer flexible, secure space in a central location. Ideal for small businesses, growing brands, e-commerce teams, and operations with high stock levels.

Enjoy complimentary 24/7 PIN-code access, off-street parking with loading bays, trolleys and pallet trucks, plus advanced security with individual intruder alarms, CCTV, and climate-secure units.

Whether you need long‑term business storage or tailored support for stock management, our service scales with your business; no fixed contracts, no hidden fees.

Get a free quote, price match, and 50% off for the first 8 weeks.

Frequently Asked Questions

What is the difference between stock management and inventory management?

Stock management focuses on finished goods ready for sale. Inventory management includes raw materials, work in progress, and finished products.

How can small businesses forecast demand effectively?

Use historical sales data, market trends, and customer behaviour to plan ahead and avoid overstocking or stockouts.

How often should I review my stock?

Check available stock regularly. Many businesses review it weekly or monthly, depending on sales volume and product type.

How does stock management affect cash flow?

Good stock management prevents money being tied up in excess stock. It helps you invest funds where they add the most value to your business.

How can HOLD self storage assist my stock management?

HOLD helps streamline your stock management by giving you quick, secure access to inventory whenever you need it.

You can scale your space up or down as demand changes, and we can accept deliveries on your behalf to keep operations running smoothly.

Our storage experts are always on hand to offer advice, help you choose the right unit size, and ensure your setup supports your day-to-day business needs.